")

georgeclerk

Introduction

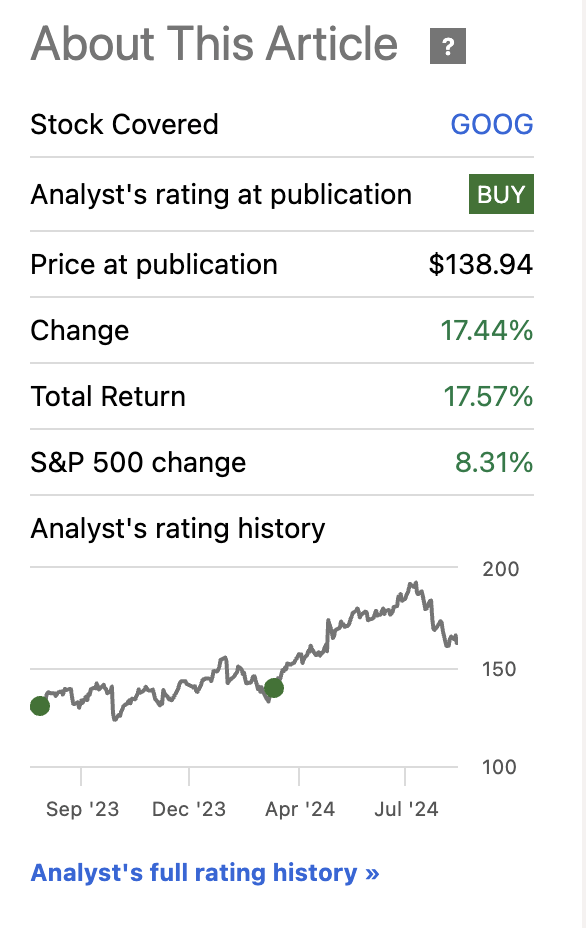

Alphabet (NASDAQ:GOOG) has taken a slight breather from climbing the price ladder, allowing me to start a small position. Below I will go through my reasons for the company’s long-term longevity.

Since my previous article, where I maintained my Buy rating because the company was the only one fundamentally undervalued out of the Fab 5. Since then, the company has seen a decent rally and outperformed the broader index. I still think the company has a lot of room for growth and even with conservative estimates, Alphabet Inc is undervalued at these prices. The dip should be viewed as a blessing for people who would like to accumulate more shares, like me.

Seeking Alpha

Search Dominance is alive and well

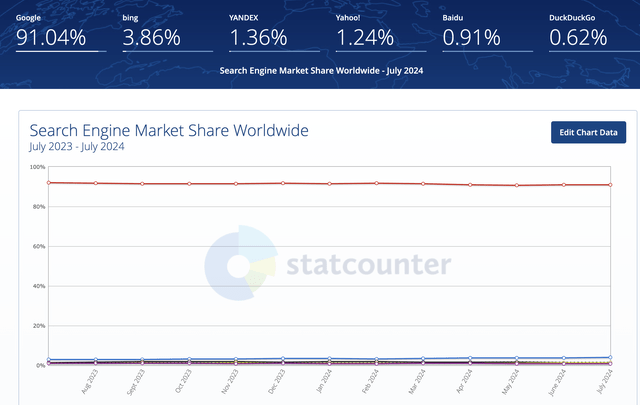

So, there has been a lot of negativity surrounding the company’s dominance in the search engine area. When Microsoft’s (MSFT) Bing got its AI-enabled search, I thought that’s it, Bing was going to replace my daily search engine. And to be honest, it did for a while. With time, I noticed the many flaws of AI-search responses. The confidence of these LLMs in what they are saying to be true was astounding. Bing AI search, now Copilot, would be looking into any articles that relate to the subject as recent no matter the date I was looking for, and present it as that’s the latest information available. The problem still stands with Gemini, the Alphabet’s AI. However, I still prefer to use Google Chrome and Gemini instead of Copilot and Bing Search. In terms of sources to cite, Copilot does a better job, I just don’t like Bing. It feels bloated and unnecessary to have all of that information on the front page when I want to just search, and not read an unnecessary news article, which is most likely a clickbait anyway. I know it can be turned off, but that should have been the default. And I am sure I am not the only one in this. Just look at the latest market share metrics.

StatCounter

It seems to me that other search engines made no dent in Google’s search dominance, and the closest one being Bing, hardly anything to brag about. I see a vocal minority praising DuckDuckGo, but I just don’t think we are going to make it a verb any time soon, like “google it” has become over the years. “DuckDuckGo it”, is too much of a mouthful. Of course, with DDG, privacy is the main reason why some people choose it, and the search neutrality, but looking at the graph above, not many people care about it to actively switch in their browser. It takes a max of 5 clicks to switch.

The company’s Google Search & other still saw a decent y/y growth, especially when you see how big the company already is. The segment saw around 14% growth y/y, so the search segment is alive and well.

Is this dominance going to change significantly over the long-term? That is a tough question no one knows the answer to. The recent lawsuit result went against Alphabet, which said that the company was using its dominance to build itself as an illegal monopoly in search and text advertising. Strong barriers of entry and a feedback loop that sustained its dominance were cited as the main reasons the judges ruled against Alphabet. The lawsuit said the company paid a lot of money to be the preferred search engine on phones using Android and Apple’s (AAPL) operating systems. So now, Alphabet is not allowed to pay Apple $26B to keep its search engine as the default choice. A lot of people seem to think that this was a good thing for GOOG. Losing is not a good thing most likely. However, saving over $20B is a lot, but how is this going to affect the company’s profitability in the long run, we are not sure yet. The company may lose some market dominance over the next few years because of it, but also, only if there are decent alternatives to the simplicity of Google search. Are people going to opt for a different search engine when prompted? I would probably select Google out of the gate if I was given a choice between Google, DuckDuckGo, Bing, and Yahoo. I know Google Search, I know how it functions, and so do a lot of people, so I still think many people will opt for it because it is familiar and easy to use. So, who knows, maybe the lawsuit outcome is a blessing in disguise. Time will tell.

Diversification of Revenues

The company is not a one-trick pony any longer. Although its bread and butter are still search and ads, GOOG has come a long way and can be seen as a lot less risky because of diversified revenues of stream that still have a lot of potential. Below are the main ones for me.

YouTube Slowly Creeping Up

I am a huge fan of the service. I’ve mentioned in my other articles that YouTube became my go-to entertainment source when I want to unwind. This segment overtook the Google Network to become the second-best revenue generator in the Google Advertising segment of revenues. YouTube Ads saw a 13% y/y growth while Google Network declined in the same period. This slow creep-up in revenues helps Alphabet diversify away from Search as being the only viable revenue generator. I would like to see it grow even faster, but the combined growth of the search and YouTube is rather decent for such a massive company. The platform is clearly on the rise still. It has remained the top choice for US households in streaming watch time, according to the latest transcript, while doubling watch time on connected TVs from a year ago. I’ve lost track of how many hours I would spend a week just swiping YouTube Shorts. The algorithm knows what I like to look at and keeps me hooked. With further improvements in quality on the platform to attract more viewers, advertising agencies will cough up more to be able to advertise, which means this revenue segment is going to continue to perform well. It will most likely not replace the company’s main revenue generator, but it will be a decent chunk in the next decade.

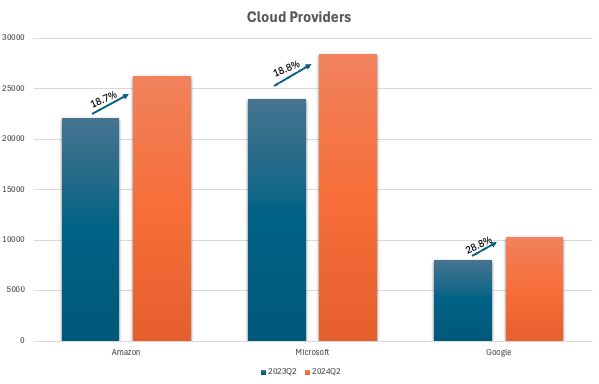

Google Cloud Growing Faster Than Competition

The company’s Cloud continues to trail the two juggernauts in this area, MSFT’s Azure, and Amazon’s AWS; however, the latest quarter report shows the revenue growth to be quite admirable. Y/y growth came in at around 29%, and if we compare it to the latest reports from the top two, we can see that GCP is growing much faster. While the top two players have very similar revenue numbers, GCP is trailing quite a bit, however, is it safe to assume the GCP will eventually reach similar numbers? If it manages to grow quicker than the competition, I will say yes, but for now, I am content with the company maintaining its third spot and gaining on its competition. If the company continues to win meaningful contracts with companies that are willing to make its cloud platform its main platform, this revenue segment will continue to bring in billions of sales, further solidifying the diversification efforts of the company, and essentially eliminating concentration risks.

Author

The Company’s Financial Position- One of the Best

Another fundamental reason I like the company is its amazing balance sheet, which is one of the best out there in terms of liquidity and solvency. In the latest quarter, Q2 ’24, Alphabet had around $110B in cash and marketable securities, against pocket change of $13.2B in long-term debt, which hasn’t changed in a while. This alone is enough to convince me the company’s financial standing is one of the most sound out there. The company’s cash pile will help it stay relevant in the Cloud, AI, and other revenue ventures and will remain one of the key technology companies in the world. Something is bound to work out if you throw enough money at it.

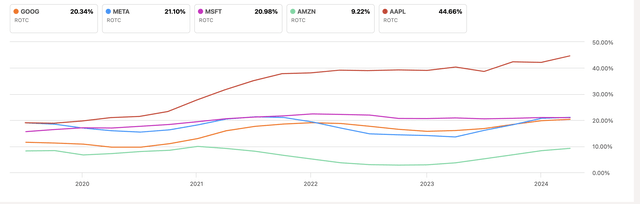

The company’s return on total capital, or ROTC, is up there with the other large-cap players, although, AAPL takes the cake.

Seeking Alpha

Does it mean AAPL is the better choice? Not to me. I think the company is quite expensive and not worth the time at the current prices. I think Meta (META) is closest to GOOG in terms of valuation, while the rest are somewhat stretched.

Valuation

Speaking of valuation, this is another reason I’m still a fan of the company. As usual, I will use what I believe to be quite conservative assumptions. For revenue growth, I went with an 8% CAGR over the next decade. In the past decade, the company managed to grow at around 18.6%, so as it is growing in size, it is natural to assume the company won’t be able to grow as it did in the past, and 8% seems achievable, if not too conservative.

Author

For margins, I decided to improve these over time, but EPS growth remains below that of what analysts are forecasting, which bodes well for my conservative outlook. I do believe that with further technological advancements, the company’s efficiency will improve. Given that the company’s Cloud is still rapidly growing and evolving, I have no doubt margins in the long run will improve.

Author

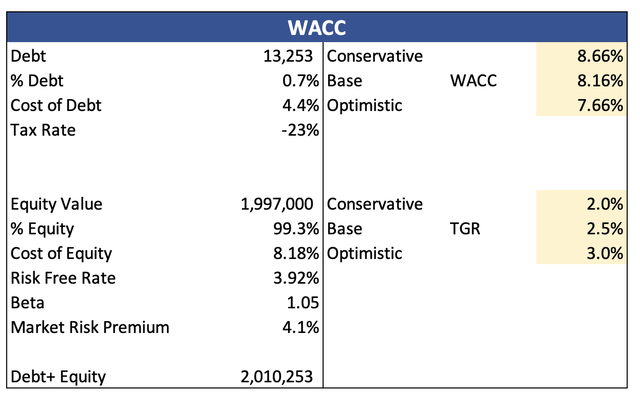

For the DCF analysis, I went with the company’s WACC of 8.16%, and a 2.5% terminal growth rate.

Author

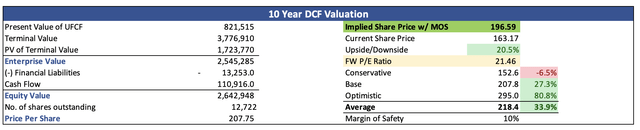

Additionally, I decided to discount the final intrinsic value by another 10% to give myself more room for errors in the estimates above. With that said, Alphabet’s intrinsic value is around $196 a share, which means it is trading at a discount to its fair value.

Author

Risks to the Thesis

In the short run, the markets have been very jittery and volatile due to an increased risk of a recession in the US. One day people are doomsayers, the next everything is fine. Furthermore, the rotation from large-cap tech stocks may rear its head once again and we will see further selling pressure in the magnificent 7 stocks and anything to do with the AI-hyped companies.

In the long run, we don’t know what the consequences of the lawsuit to the company’s top line will end up being. There could be a decent drop in the search revenue, or it is all going to be a nothingburger and people will still opt to use Google as their main search engine.

All of the hype surrounding AI means there is a lot of competition from large and small companies to come up with the best use. If the company falls behind on some of the promises of its AI, it would be hard to compete further, no matter how much capital you throw at it.

Any further lawsuits regarding its monopoly in search is going to cause more volatility in the stock price, and the company’s top-line potential could suffer.

Closing Comments

In my opinion, the risk/reward in the long run is very enticing at these levels. The reasons laid out are why I am comfortable with having this company in my portfolio for the long run. If we see further downward pressure on prices, I will not hesitate to increase my position since what I have right now is quite small. The reason it’s small is because I am not happy with the way the markets playing out right now and I will gladly take a wait-and-see approach over the next few months. There have been so many days where an index would move 4% or more from the lows/highs of the day and that is not what I like to see.

I don’t see how this juggernaut is going to stop dominating the internet search any time soon. However, we don’t know what is in store for us in the future. There may be a more appealing, easy-to-use engine that would take off, but for now, my bet is on Google.

link