US consumers’ income, spending, and savings provides a picture of their financial health. We analyzed data from the US Bureau of Economic Analysis (BEA), specifically that which was provided in Table 2.1. Personal Income and Its Disposition.

Overall, the Q2 2024 BEA data presents a mixed picture of US consumer financial health. While income is rising, driven largely by compensation from employment and government transfers, the increase in outlays — particularly in interest payments — and the sharp decline in savings are areas of concern.

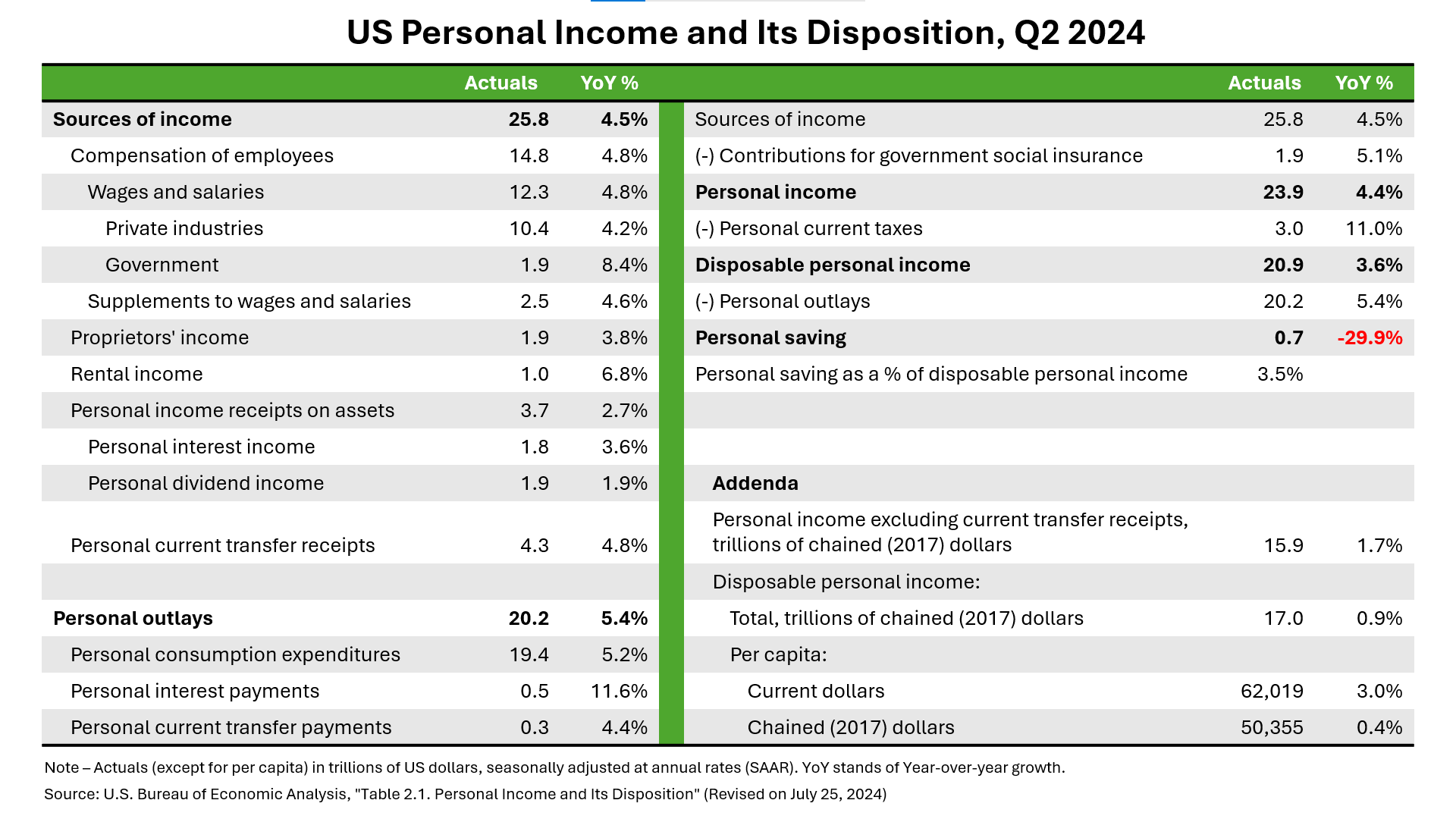

What are the factors involved? In Q2 2024, US consumers’ total personal income reached $23.9 trillion on a seasonally adjusted annual rate basis — that’s 4.4% year-over-year (YoY) growth (see figure below). Disposable personal income reached $20.9 trillion, up 3.6% YoY. The sources of personal income and their growth in Q2 2024 are as follows:

- Wages and salaries accounted for $12.3 trillion (4.8% YoY growth). Within this category, the private sector contributed $10.4 trillion. Additionally, government wages surged 8.4% YoY to $1.9 trillion, reflecting strong growth in public sector employment. Wages and salaries continue to grow faster than inflation.

- Supplements to wages and salaries amounted to $2.5 trillion, growing 4.6% YoY. These include employer contributions for pensions and insurance as well as government social insurance. Both saw healthy growth, indicating robust employer-sponsored benefits.

- Proprietors’ income with inventory valuation and capital consumption adjustments stood at $1.9 trillion, growing 3.8% YoY. Non-farm proprietors’ income from small businesses and self-employment showed solid growth, while farm income declined sharply, highlighting challenges in the agricultural sector.

- Rental income of persons with capital consumption adjustment was $1.0 trillion, up 6.8% YoY. This increase was driven by a strong rental market, contributing to overall income diversification for consumers.

- Personal income receipts on assets totaled $3.7 trillion. That includes (A) interest income at $1.8 trillion, growing 3.6% YoY and (B) dividend income at $1.9 trillion, rising 1.9% YoY. The slower growth in dividend income may be due to cautious corporate dividend policies.

- Personal current transfer receipts were $4.3 trillion, which increased 4.8% YoY. This figure was driven by an increase in Social Security benefits and Medicare.

In Q2 2024, US consumers’ total personal outlays amounted to $20.2 trillion, up 5.4% YoY. The growth in personal outlays continues to outpace the growth in personal income. The key personal outlays and their growth in Q2 2024 are as follows:

- Personal consumption expenditures were $19.4 trillion, growing by 5.2% YoY, indicating strong consumer spending on goods and services.

- Personal interest payments (non-mortgage interest) increased sharply to $0.5 trillion, rising 11.6% YoY, which signals concerns about growing consumer debt. The trend of increasing debt could strain household finances if income growth does not keep pace with the rising cost of debt.

- Personal current transfer payments totaled $0.3 trillion, growing at a modest pace of 4.4% YoY.

US consumers’ total savings declined sharply in Q2 2024. This decline raises concerns about the following:

- Personal saving (calculated by subtracting personal outlays from disposable personal income) dropped to $0.7 trillion, marking a significant 29.9% YoY decline. The decline in savings leaves consumers more vulnerable to economic shocks, as they have less of a financial cushion to fall back on.

- Personal saving as a percentage of disposable personal income fell to 3.5%, indicating a reduced consumer ability to save.

In real (inflation-adjusted) terms (or chained (2017) dollars):

- Real personal income excluding current transfer receipts was $15.9 trillion, growing a modest 1.7% YoY. This indicates that much of the income growth is driven by government benefits rather than organic growth in wages and salaries.

- Real disposable personal income was $17.0 trillion, growing by only 0.9% YoY. This means that after adjusting for inflation, consumers’ purchasing power has barely increased, potentially constraining future spending and economic growth.

- Real disposable income per capita was $50,355, growing by only 0.4% YoY. This indicates that the average consumer isn’t seeing substantial real income gains.

In our newly published report, Consumer Spending And The Economy Grow Despite Persistent Pessimism, we discuss the state of the US economy in H2 2024 and its implications for brands. US macroeconomic indicators are strong, and the US economy continues to avert a slowdown. Yet despite the abundance of good news, consumer sentiment is at a 2024 low (per University of Michigan’s July Index of Consumer Sentiment), driven primarily by a widening gap in confidence between more affluent and less affluent consumers. Our report helps marketers and strategists disentangle the complex economic environment to craft a growth strategy that addresses pricing, affordability, and value. If you are a Forrester client and would like to learn more, please schedule an inquiry or guidance session with Dipanjan Chatterjee or me!

link