/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GLB3CWXPBJETFP7KMI2PD2SUFU.png "Why Investors Missed Out on 15% of Total Fund Returns")

Imagine you invest in a fund. Over the next 10 years, it generates a 7.3% total return per year after fees. Not bad. But when you check your brokerage statement and do the math, you find you earned about 1.1 percentage points per year less than that. What gives?

A fund’s total return assumes an initial lump-sum purchase that’s held until the end. But that’s not how you invested. You made an initial purchase, added to it, withdrew a chunk, sold a bit more, then made a final buy. Thus, your return won’t be the same as the buy-and-hold return. It’ll be whatever your average dollar earned, given the timing and amount of those buys and sells. If you buy high and sell low, your return will lag the buy-and-hold return. That’s why your return fell short.

Mind the Gap

We’ve been studying this phenomenon—which we call the “Investor Return Gap”—for nearly two decades. Today, we published our latest installment of the research, finding that investors lost out on around 15% of the returns their fund investments generated over the 10 years ended Dec. 31, 2023, as explained further below.

Here are the key takeaways from this year’s “Mind the Gap” study:

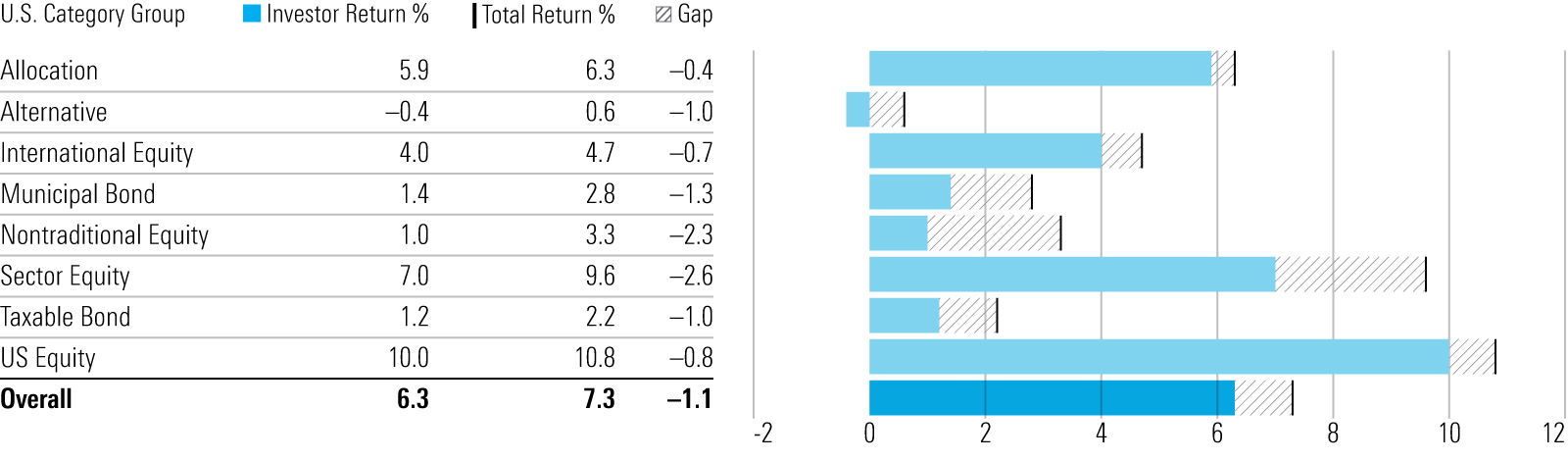

- Fund investors earned a 6.3% per year dollar-weighted return (“investor return”) over the 10 years ended Dec. 31, 2023, while their fund holdings earned about 7.3% per year (“total return”).

- Encouragingly, investors earned high dollar-weighted returns in popular fund types like US equity (10% investor return per year) and allocation (5.9% annually); on the flip side, alternative funds were the only fund type that failed to generate a positive investor return over the study period.

- The 1.1-percentage-point annual estimated return gap—which is equivalent to around 15% of funds’ aggregate average total return—is broadly in line with the gaps measured over the rolling 10-year periods ended in December 2019, 2020, 2021, and 2022.

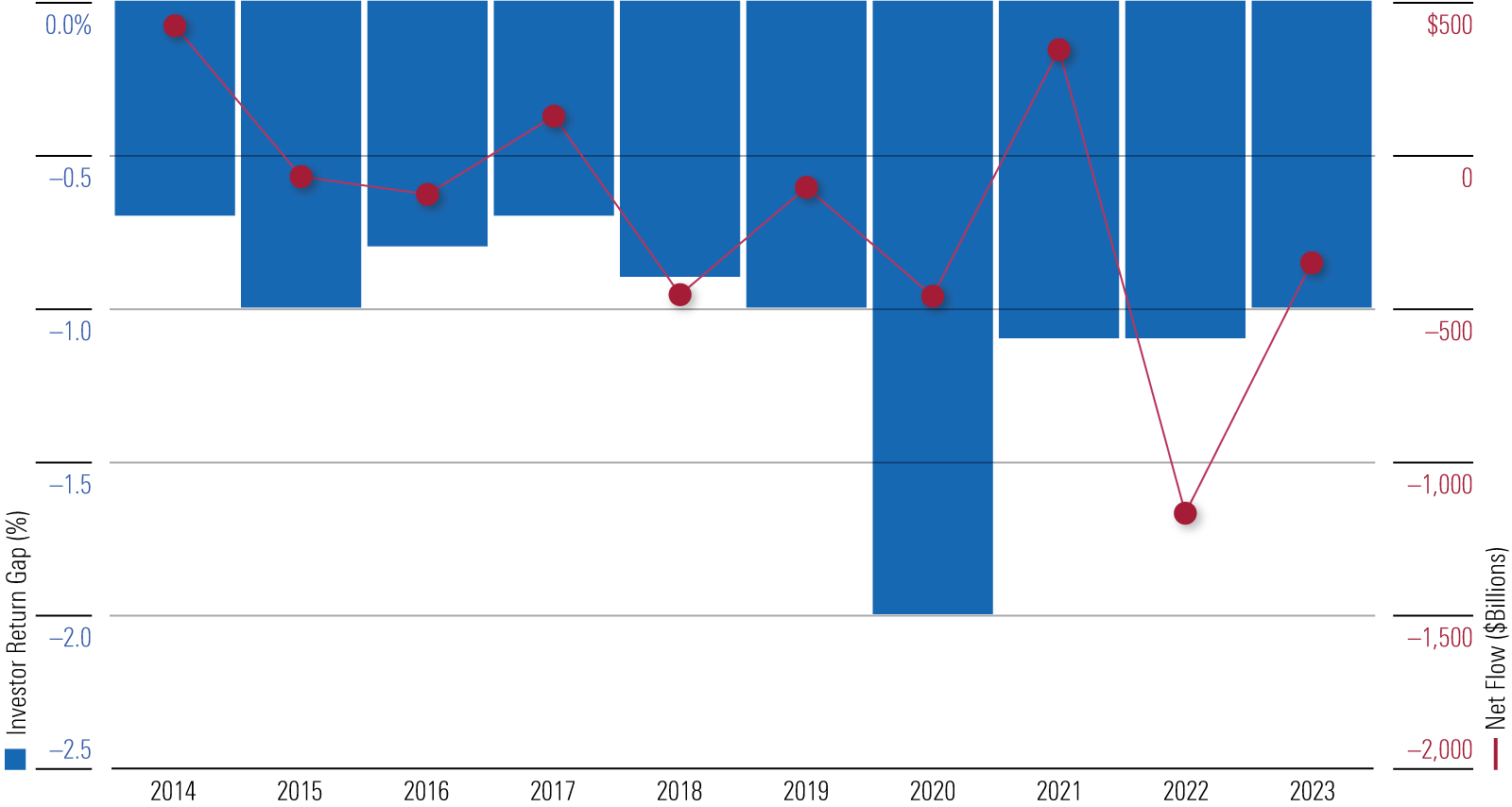

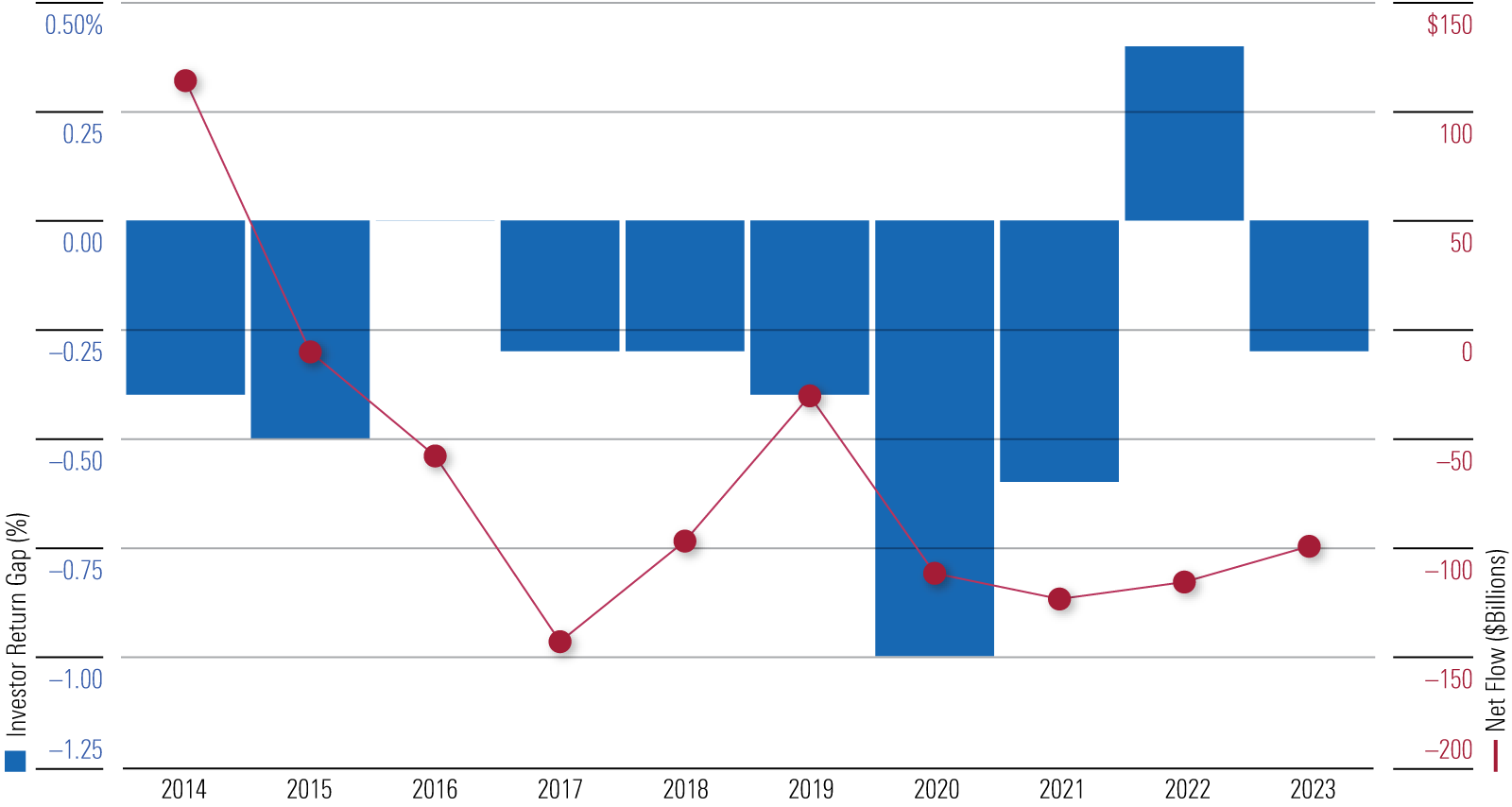

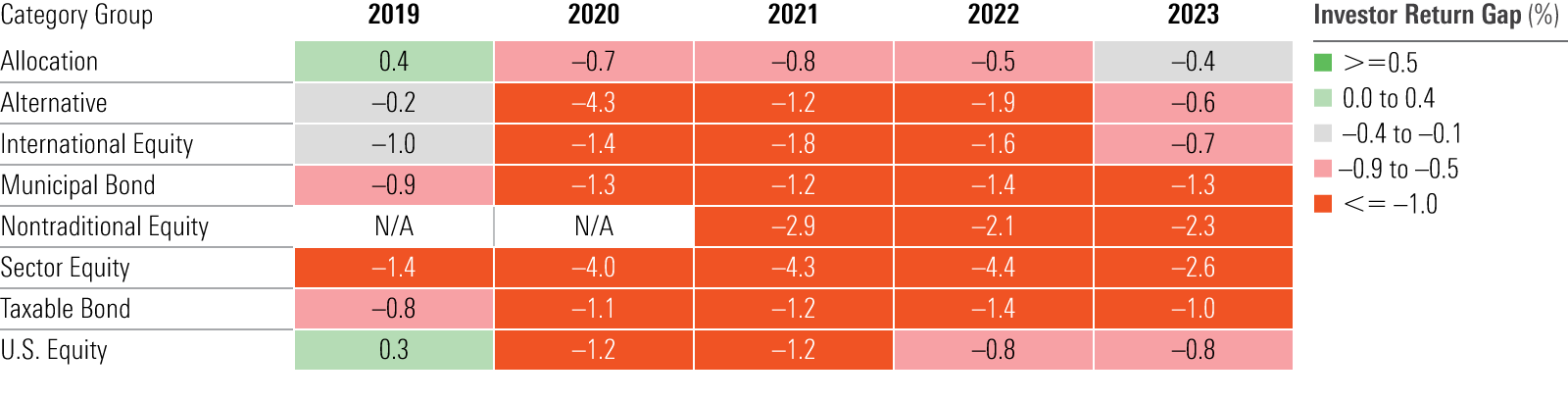

- The average dollar’s return lagged the average total return in all 10 of the calendar years in the study period; investors appear to have incurred heavy timing costs in 2020 (leading to a gap of negative 2 percentage points that year).

- Allocation funds had the narrowest gap (negative 0.4 percentage points per year over the 10 years ended Dec. 31, 2023, which is less than half the gap for funds as a whole). This means allocation fund investors kept significantly more of their returns than investors did in other category groups.

- This continues a consistent pattern in which investors in all-in-one, multi-asset strategies have captured the largest portion of their funds’ total returns; conversely, sector equity funds had the widest gap (lagging by negative 2.6 percentage points annually), which echoes our findings in previous studies.

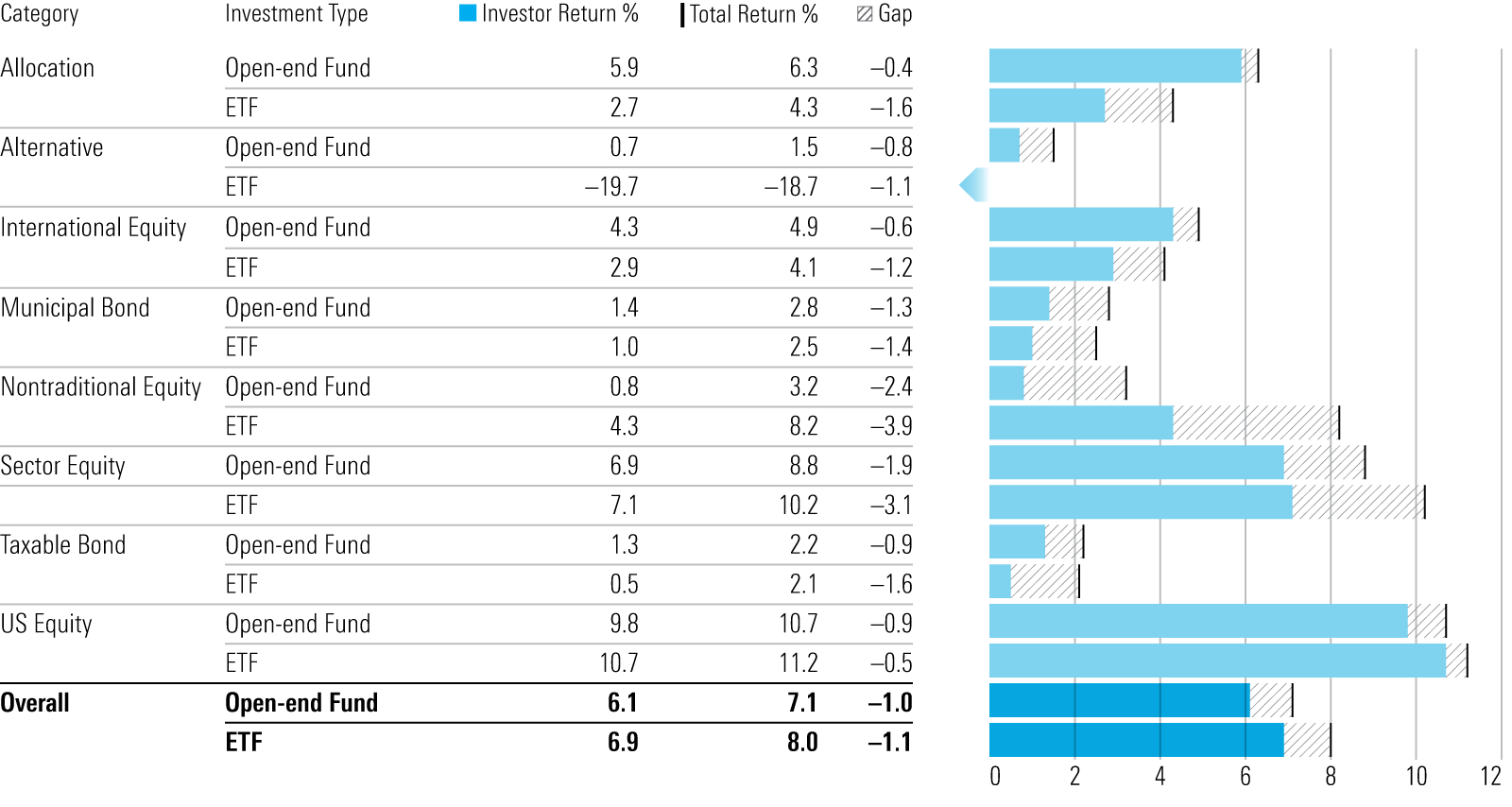

- Open-end funds earned a 6.1% investor return per year (a gap of negative 1.0 percentage points) versus 6.9% for ETFs (a gap of negative 1.1 percentage points); gaps were generally narrower for open-end funds than ETFs even when we controlled for asset class.

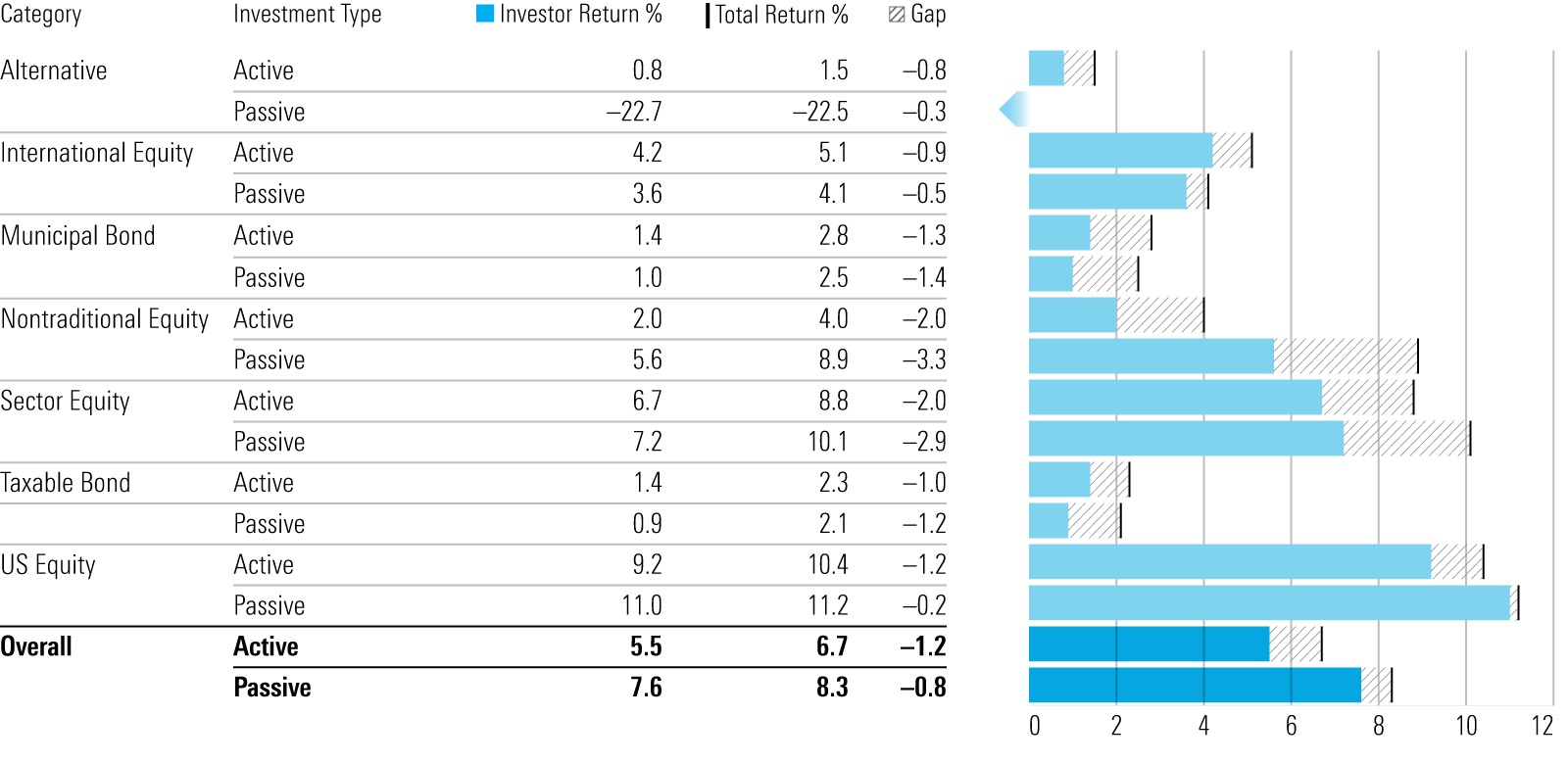

- The average dollar invested in index funds earned a 7.6% annual return (negative 0.8-percentage-point gap) compared with 5.5% per year in active funds (negative 1.2-percentage-point gap).

- While there was a small gap for index mutual funds over the 10-year period (negative 0.2% per year), that wasn’t true of index ETFs, where the average dollar earned 1.1% less per year than the buy-and-hold return.

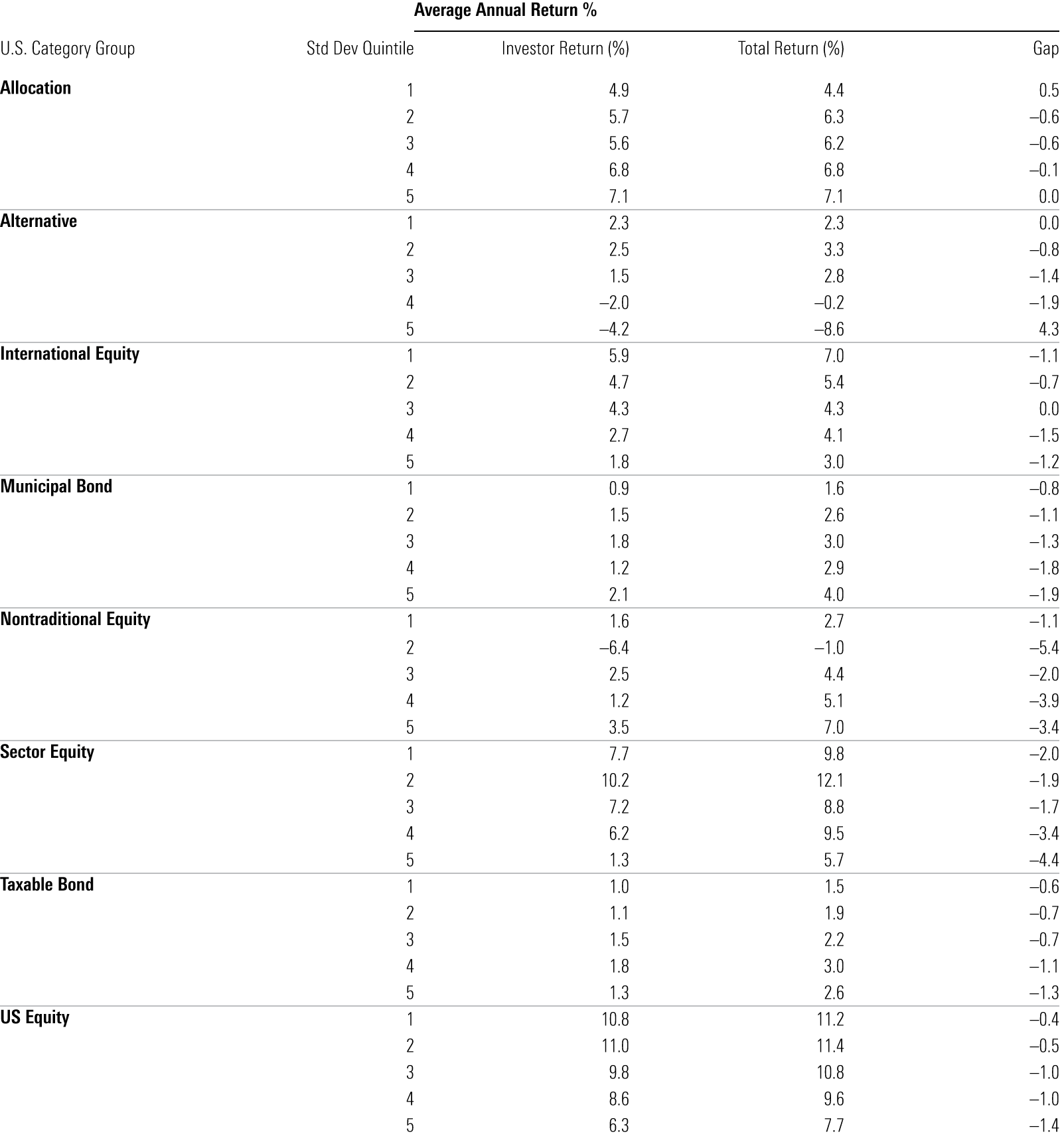

- The more volatile a fund’s returns versus peers, the larger the gaps tended to be; the average dollar invested in the most volatile sector equity funds lagged the buy-and-hold return by over 7 percentage points per year.

6 Routes to Closing the Gap

How can investors capture a greater share of their funds’ total returns in the future? The study’s findings yield some insights into that.

- Less is more: Investors seem to have enjoyed greater success using widely diversified, all-in-one allocation funds. And why? There are multiple reasons, but these strategies automate mundane tasks like rebalancing. That means less transacting, and less transacting appears to have conferred higher dollar-weighted returns than otherwise.

- Context counts: Allocation funds are often used in defined-contribution plans. This mechanizes investing, avoiding the potentially large timing costs investors can incur when making large, ad hoc transactions. Narrower funds, like sector equity strategies, aren’t typically offered in such contexts and thus see more irregular transactions that can dent dollar-weighted returns.

- Routine helps: Although not directly addressed in the study, the findings imply that routinized investing, such as making regular contributions to a retirement plan, can itself be helpful in capturing more return. The more investors can mechanize saving and investing, the less likely it is they’ll engage in costly trading activity. In that sense, it’s addition by subtraction.

- Volatility hurts: Again and again, we’ve found that investors struggle to use volatile funds successfully. They chase returns to their detriment, and this holds even when we limit the comparison to funds of the same general type. The more a strategy rattles around, the more likely it is to leave investors shaken.

- Maintenance not needed: Narrow funds are usually more volatile by their very nature, and our findings suggest a link between higher volatility and wider investor return gaps. But volatility aside, these strategies are usually higher maintenance, forcing investors to make buy or sell decisions at what can be fraught times.

- Convenience comes at a cost: The gap between index ETFs’ dollar-weighted returns and their total return was wider than the gap for index open-end funds. ETFs don’t enjoy the benefit of being directly available in 401(k) plans or being holdings in target-date funds that are fixtures of such plans. But it does raise the question of whether the convenience ETFs afford—that is, the ease with which they can be bought and sold—comes at a cost.

Conclusion

Our annual “Mind the Gap” study finds that investors captured a large chunk of their funds’ total return over the 10 years ended Dec. 31, 2023, but not all of it. The 1.1% annual gap is significant, amounting to around 15% of the total return funds’ generated in aggregate over this span. Investors could capture more of their funds’ total returns by holding the line on transactions, perhaps by opting for widely diversified, all-in-one options like allocation funds that automate certain tasks while avoiding narrower, volatile strategies that are harder to handle.

The author or authors do not own shares in any securities mentioned in this article.

Find out about Morningstar’s editorial policies.

link