")

gremlin/E+ via Getty Images

Zscaler (NASDAQ:ZS) is one of the few software names to show strength amidst macro headwinds and also have a stock still trading at reasonable valuations. With many tech names having to lower full-year guidance due to muted headcount growth among their customers, ZS continues to “beat and raise” like it’s business as usual. The company has a net cash balance sheet and generated its first quarter of GAAP net profitability. The stock trades with the typical premium associated with cybersecurity stocks, but not nearly to the same degree as others. In spite of some salesforce attrition, the stock still looks poised to deliver market-beating returns – I reiterate my buy rating for the stock.

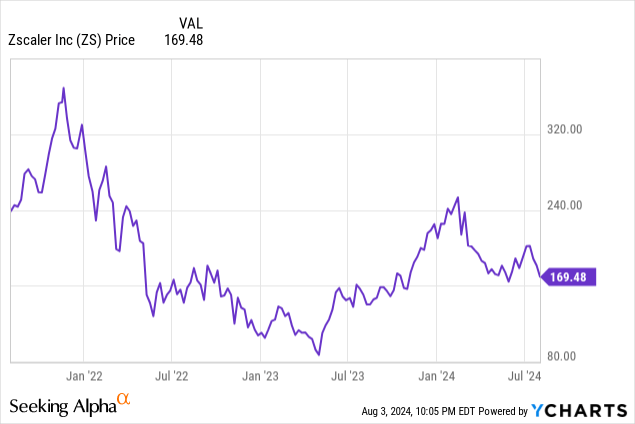

ZS Stock Price

I last covered ZS in April where I explained why I was upgrading the stock to buy after the stock had sold off amidst market volatility.

Given the strong financial results, I’m surprised that the stock has not performed stronger than it has. Even without a re-rating to the lofty levels which Crowdstrike (CRWD) trades at, the stock still looks attractive here.

ZS Stock Key Metrics

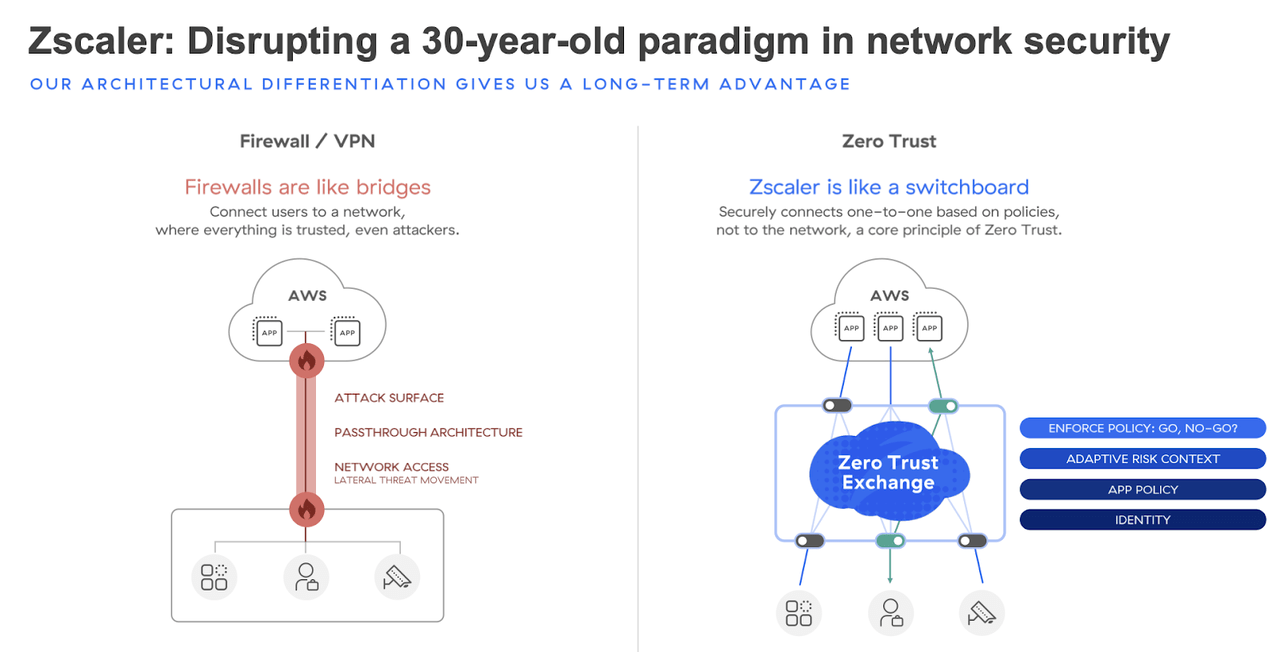

ZS is an enterprise tech company in the cybersecurity sector. Its products aim to disrupt the legacy firewall security model by instead securing apps and data on a one-to-one level based on policies and not the network.

FY24 Q3 Presentation

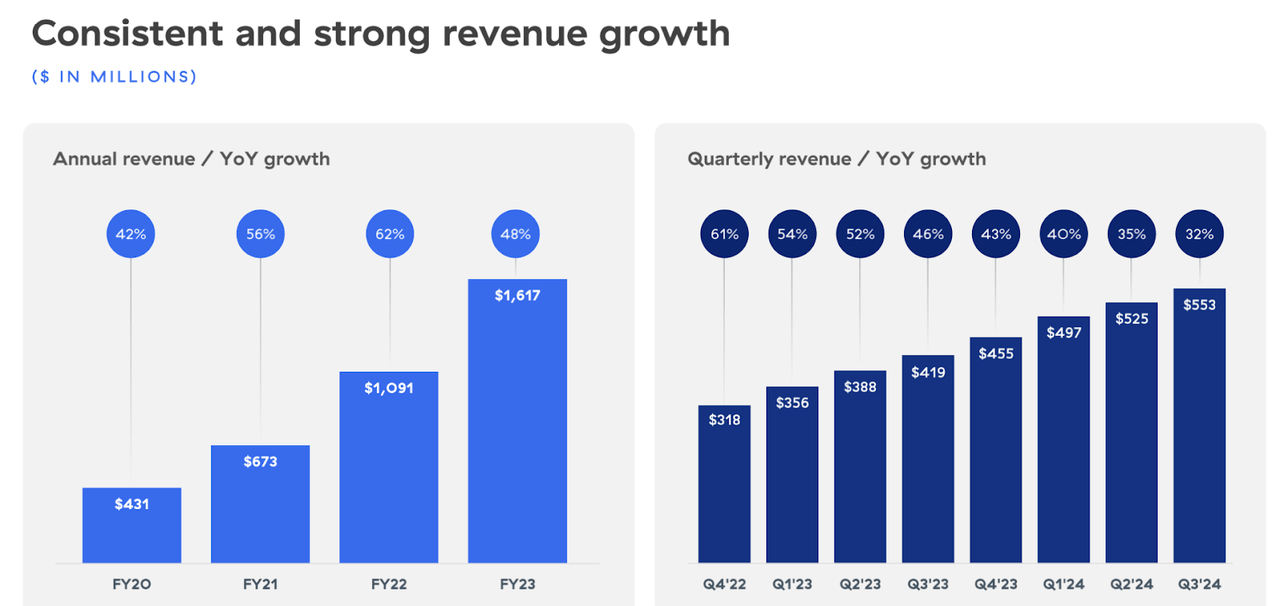

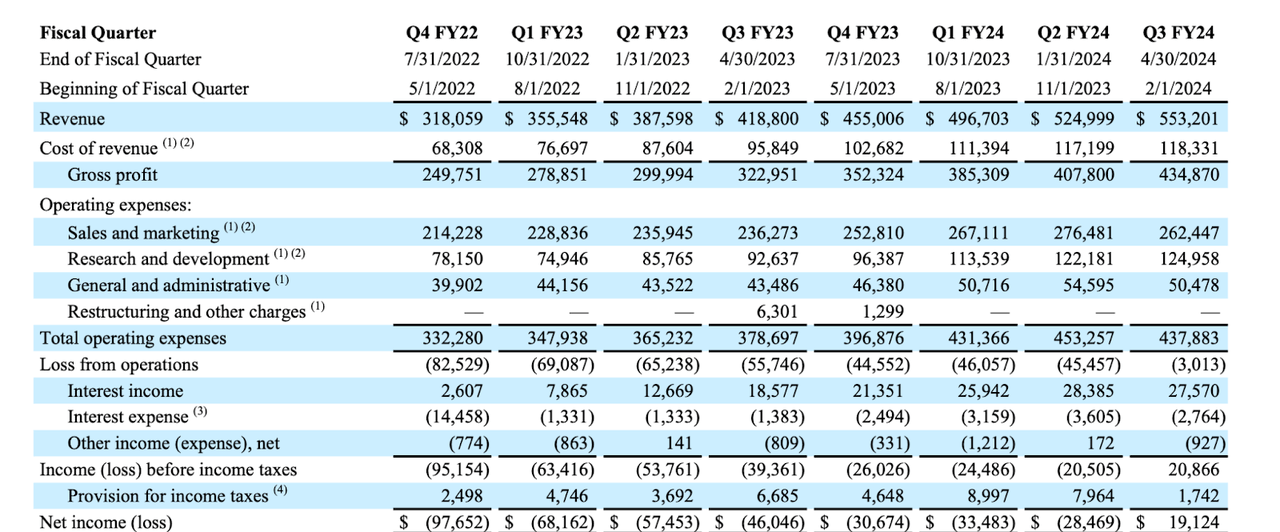

In its most recent quarter, ZS delivered 32% YoY revenue growth to $553 million, surpassing guidance for up to $536 million. It is impressive that ZS continues to deliver such aggressive top-line growth even after it passes post-pandemic comps and deals with the higher interest rate environment. The company’s 116% dollar-based net expansion rate was particularly impressive given that most software peers have indicated that customers are more hesitant on hiring due to waiting to see the effects of generative AI. It is possible that ZS benefits from having a platform portfolio, giving it more products to upsell to customers, and its cybersecurity positioning makes its products “mission critical.”

FY24 Q3 Presentation

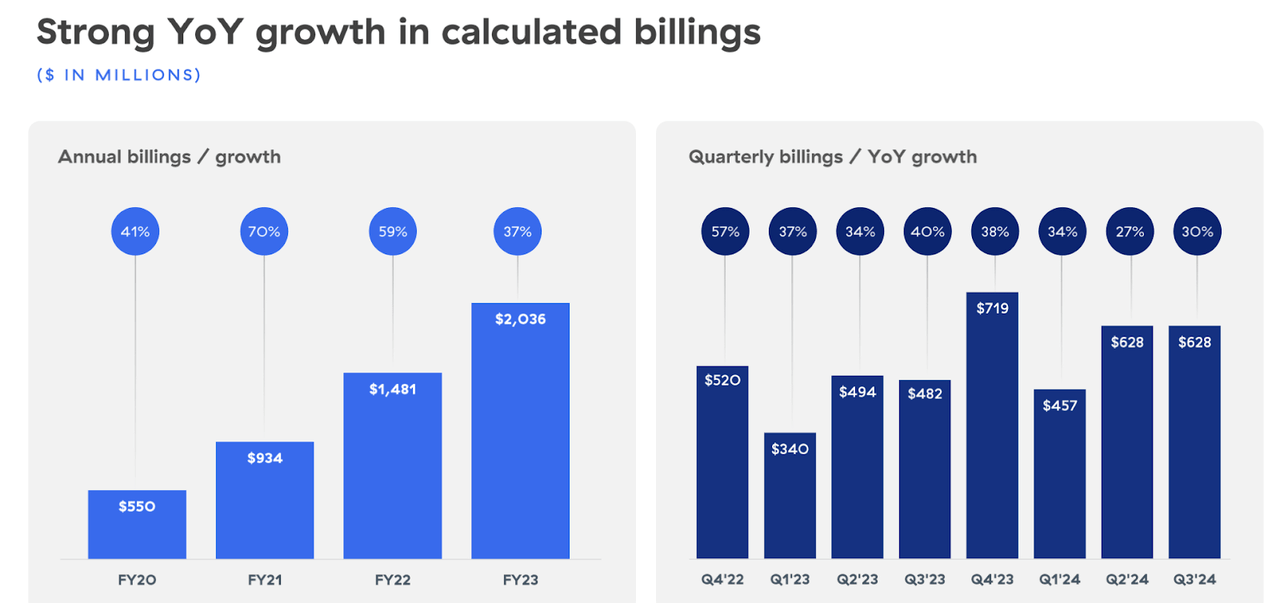

The company also generated 30% YoY billings growth to $628 million as well as 29% YoY growth in current billings, which may indicate that the company can sustain aggressive growth rates moving forward.

FY24 Q3 Presentation

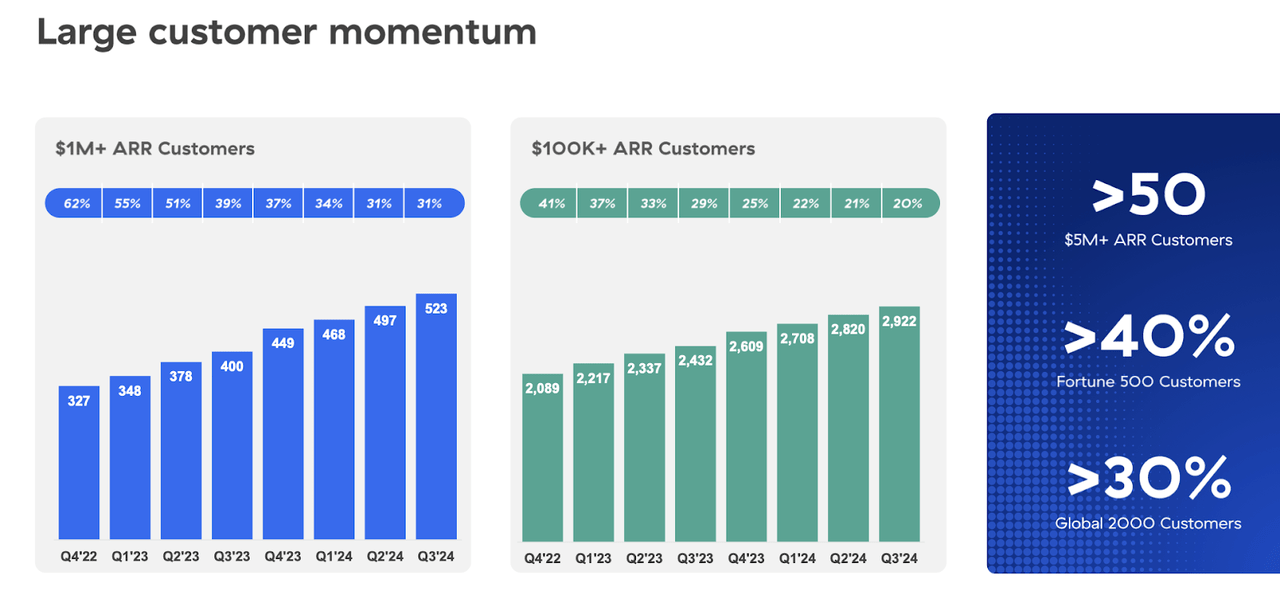

ZS continued to rapidly add customers – in today’s environment marked by higher interest rates and generative AI headwinds, the perks of a leading operator within the cybersecurity sector can not be understated.

FY24 Q3 Presentation

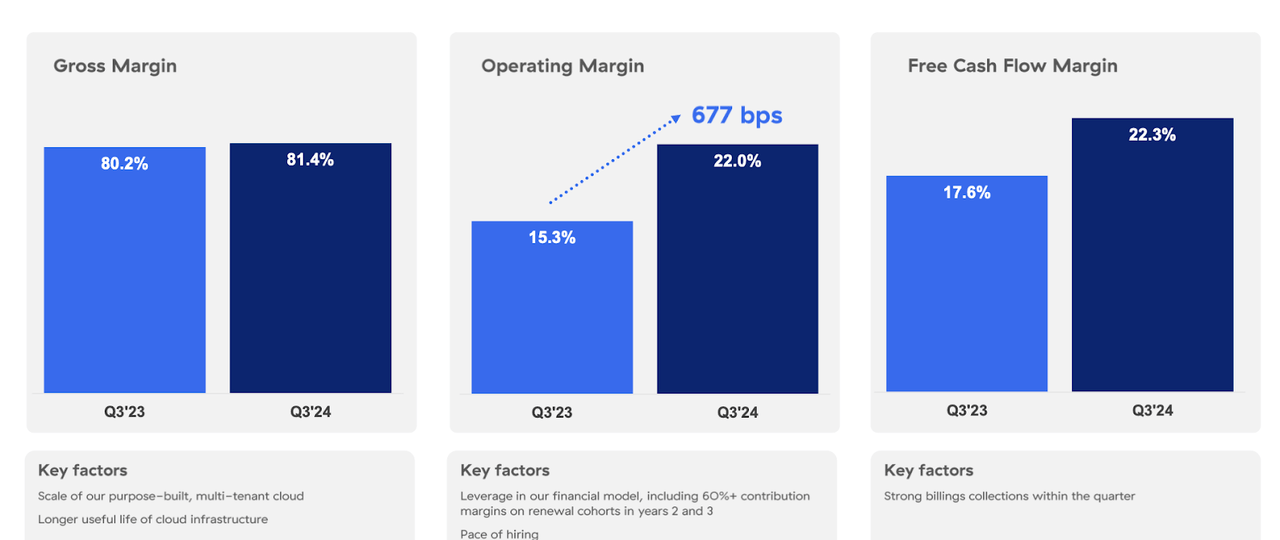

On the profitability front, ZS generated $122 million in non-GAAP operating profits, surpassing guidance for $100 million and representing a 22% margin.

FY24 Q3 Presentation

It is notable that ZS cut its GAAP operating loss from $55.7 million last year to $3 million in this quarter, and due to interest earned from its corporate cash, was able to generate a positive quarterly GAAP net profit for the first time. Due to the company’s high gross margins, I expect it to make further inroads on profitability moving forward.

FY24 Q3 Presentation

ZS ended the quarter with $2.2 billion of cash versus $1.1 billion of debt, representing a strong net cash balance sheet.

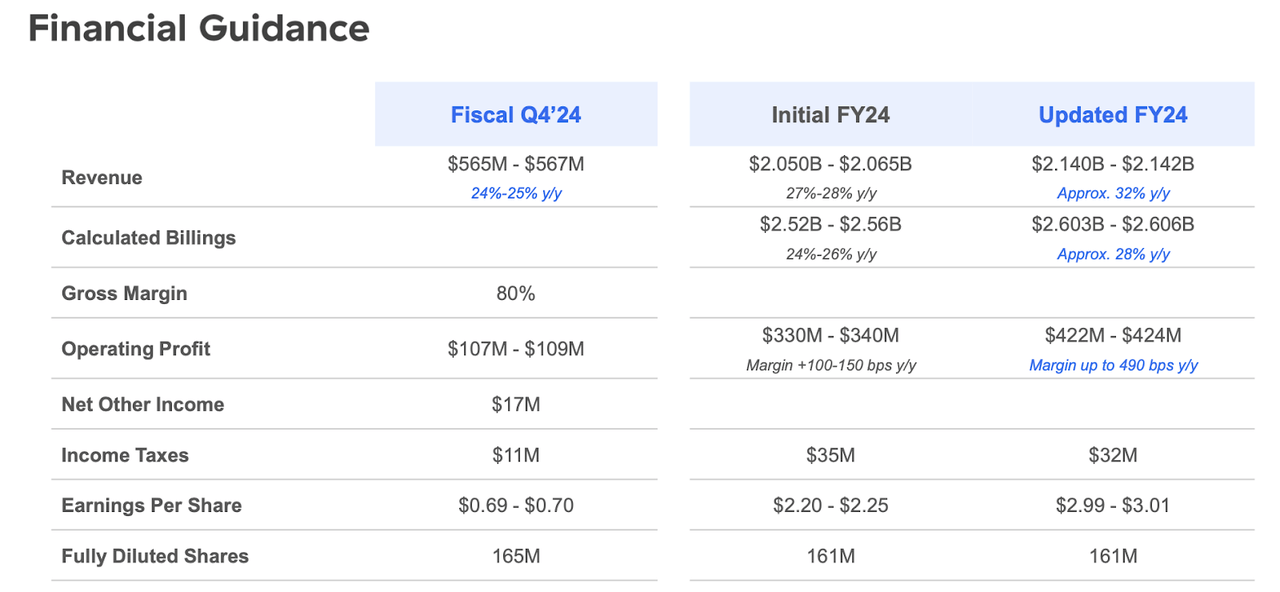

Looking ahead, management has guided for the fourth quarter to see only 25% YoY revenue growth to $567 million, representing somes sequential deceleration.

FY24 Q3 Presentation

On the conference call, management blamed the projected slowing growth rate on elevated attrition in their sales teams, which may have been due to the departure of their COO. Management believes that they will be able to correct these issues, though it may take some time. When asked if they might increase their focus on profitability amidst the temporary slowdown in growth, management explicitly emphasized that growth remains their primary focus. Management noted that profitability will come naturally as operating leverage takes hold, going as far as saying that “there’s no reason really to focus on operating profitability.” I know many tech names which would kill to have that kind of confidence in this environment. As they did in prior quarters, management noted that their dollar-based net expansion rate may continue to compress due to them having greater success in selling bigger bundles upfront, but who is going to complain when they are still generating such aggressive growth rates?

Is ZS Stock A Buy, Sell, or Hold?

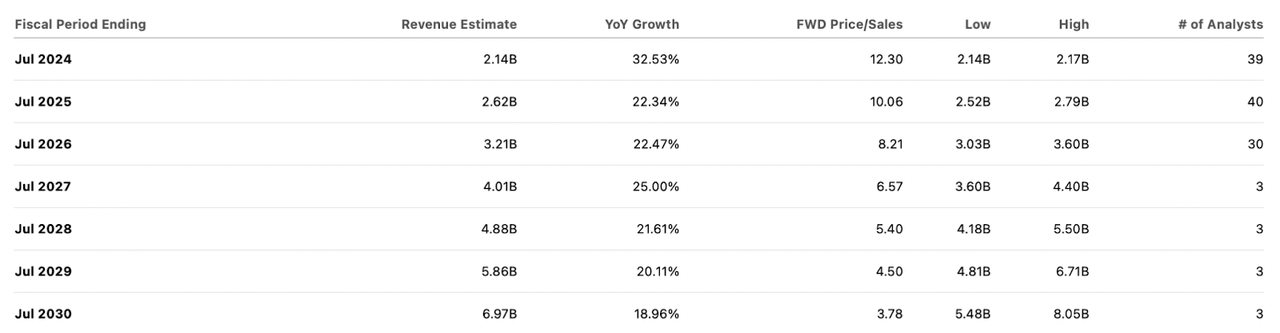

Even accounting for the projected sequential deceleration in growth (to a still-astounding 25% rate), these results were very strong and one would think that the stock would have soared. Instead, the stock still trades at reasonable valuations of around 12x sales. In contrast, CRWD trades at well over 13x sales (and was at the 20x range prior to the outage) and names like Palo Alto Networks (PANW) and CyberArk (CYBR) trade at comparable valuations in spite of materially slower growth rates.

Seeking Alpha

While I can see ZS trading at even higher multiples as it continues to boost profit margins, I will not factor that for modeling purposes. I can see ZS generating well over 40% net margins over the long term, but will assume 35% for some conservatism. That places the current valuation at around 35x long term earnings, which looks more than reasonable given the projected 20+% growth rate for years to come. Even factoring some multiple compression to the 11x sales range, ZS still looks priced to deliver well over 20% annual returns moving forward.

ZS Stock Risks

One of the allures of ZS is its ability to sustain such rapid top-line growth, but that might be a future risk. As noted earlier, management has been hinting that faster sales may lead to lower expansion rates in the future. It is possible that revenue growth may decelerate faster than anticipated. It is not clear how generative AI might impact the cybersecurity space – it is possible that ZS is somehow disrupted by future competition. ZS and cybersecurity stocks in general trade at a premium to tech peers. It is possible if not likely that this premium fades over time, which may lead to volatility for ZS stock (I note that ZS traded like a “normal” tech stock for much of 2023).

ZS Stock Conclusion

ZS comes with some premium, but that premium looks deserved given the aggressive top-line growth, net cash balance sheet, and strong profitability. I expect ZS to continue making in-roads on GAAP profitability even if management appears to not be focused on that front. The stock trades at a discount to cybersecurity peers on a growth adjusted basis but is also looking attractive in its own right. I reiterate my buy rating for the stock.

link